ROYAL Dutch Shell has provided a boost for the hard-pressed North Sea oil and gas industry by announcing plans to revamp the huge Penguins field off Shetland.

The Anglo Dutch giant confirmed it has given the green light to a project that will involve it making a hefty investment alongside America’s ExxonMobil.

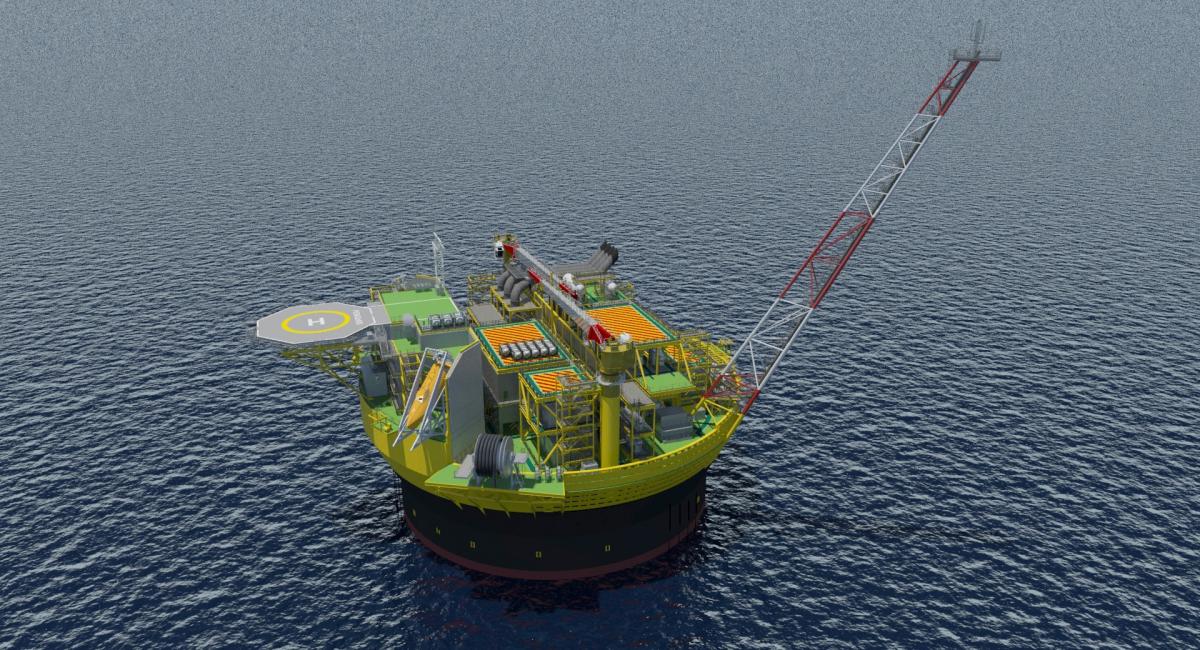

Shell expects to be able to make good money from the development at current crude prices using a giant new production vessel.

The company said the proposed investment showed the North Sea remained an important area to it. Led by chief executive Ben van Beurden, Shell has retrenched in the area in response to the oil price fall since 2014.

Shell has sold off a big chunk of its North Sea business and shed more than 1,000 North Sea jobs. In November 2016 the firm said it would close its accounts centre in Glasgow, putting nearly 400 posts at risk.

“Having reshaped our portfolio over the last twelve months, we now plan to grow our North Sea production through our core production assets,” said Steve Phimister, who runs Shell’s business in the area.

News of the development will be welcomed across the oil and gas supply chain following three years of grim trading conditions in the North Sea. Cuts in spending on new developments have taken a heavy toll on the oil services sector.

Shell’s decision will encourage hopes that brighter times are in prospect in the North Sea. The partial recovery in the crude price in the last 15 months has boosted sentiment. Industry leaders say cost cutting moves by oil and gas firms have helped boost the competitiveness of the area.

The chief executive of trade body Oil & Gas UK, Deirdre Michie, said: “A global leader like Shell making a commitment on this scale demonstrates the investment potential the UK Continental Shelf still holds.”

She added: “We are hopefully entering a more positive phase for our industry in the UK with new projects on the horizon that I hope will bring a much needed boost for companies in the supply chain.”

Wood Mackenzie said last week 14 North Sea projects were in the running for approval in the final investment decision process, including Penguins. Fiona Legate, senior research analyst at the consultancy said of Penguins: "This is the largest FID since Culzean in August 2015 and shows market confidence has returned."

But projects up for approval are not on the scale of the giant developments completed by Shell and BP West of Shetland in recent years, which were sanctioned amid the boom that ended in 2014.

Shell expects to develop a sophisticated floating production storage and offloading vessel to handle the output from Penguins and to drill a series of wells. The field lies 150 miles north east of Shetland.

Around 400 people are expected to work on the project during the construction phase, across the supply chain. Fifty or more will work on the production vessel when it is operational.

Shell hopes production will start in the early 2020’s and peak at around 45,000 barrels oil equivalent daily.

It said: “The redevelopment is an attractive opportunity with a competitive go-forward break-even price below $40 per barrel.”

Bank of America Merrill Lynch yesterday upped its forecast for average Brent crude oil prices this year to $64/bbl, from $56/bbl. It noted moves by Opec members to cut production to support the market, improving cyclical conditions and cold winter weather.

The bank expects Brent to average $55/bbl to $65/bbl over the next five years, with strong US shale output likely to impact on prices.

Brent sold for around $69.75/bbl yesterday, against less than $30/bbl early in 2016. It fetched $115/bbl in June 2014 before growth in global supplies ran ahead of demand.

Penguins was brought onstream in 2002. Output is routed via facilities on the Brent field, which is in the decommissioning process.

Shell and ExxonMobil both have 50 per cent stakes in Penguin.

Why are you making commenting on The Herald only available to subscribers?

It should have been a safe space for informed debate, somewhere for readers to discuss issues around the biggest stories of the day, but all too often the below the line comments on most websites have become bogged down by off-topic discussions and abuse.

heraldscotland.com is tackling this problem by allowing only subscribers to comment.

We are doing this to improve the experience for our loyal readers and we believe it will reduce the ability of trolls and troublemakers, who occasionally find their way onto our site, to abuse our journalists and readers. We also hope it will help the comments section fulfil its promise as a part of Scotland's conversation with itself.

We are lucky at The Herald. We are read by an informed, educated readership who can add their knowledge and insights to our stories.

That is invaluable.

We are making the subscriber-only change to support our valued readers, who tell us they don't want the site cluttered up with irrelevant comments, untruths and abuse.

In the past, the journalist’s job was to collect and distribute information to the audience. Technology means that readers can shape a discussion. We look forward to hearing from you on heraldscotland.com

Comments & Moderation

Readers’ comments: You are personally liable for the content of any comments you upload to this website, so please act responsibly. We do not pre-moderate or monitor readers’ comments appearing on our websites, but we do post-moderate in response to complaints we receive or otherwise when a potential problem comes to our attention. You can make a complaint by using the ‘report this post’ link . We may then apply our discretion under the user terms to amend or delete comments.

Post moderation is undertaken full-time 9am-6pm on weekdays, and on a part-time basis outwith those hours.

Read the rules hereLast Updated:

Report this comment Cancel